|

|

|

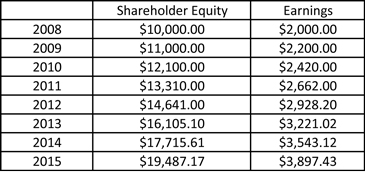

A High Return on Equity (ROE)In addition to consistent and growing earnings, a high return on equity (ROE) is one of the most important characteristics of a business. ***z-affiliate-ad-1.shtml*** A high return on equity is usually a sign of good corporate management and the superior economics of a great business. So, as a general rule, you want to own companies that generate high returns on equity. What is Return on Equity (ROE)?Let's divide this question into two parts... First, let's define equity. Shareholder equity is simply a company's assets subtracted by its liabilities. Hopefully, when the math is done, a positive number is leftover. That number is shareholder equity. It's really no different than home equity. Let's say you purchase a house for $200,000. Five years later, you've paid $40,000 on your $200,000 mortgage and the house is appraised for $300,000. Since the house is assessed at $300,000 and you now owe only $160,000, your home equity is $140,000. $300,000 - $160,000 = $140,000 Shareholder equity is calculated the same way. Let's say your company has inventory, accounts receivable, plant, equipment and other assets equal to $20,000. It also has accounts payable, long-term debt, and other liabilities equal to $10,000. In such a scenario, shareholder equity is $10,000. $20,000 - $10,000 = $10,000 Now, let's say your company has $2,000 in earnings for the current year. This is your return. Since your company earned a $2,000 return on $10,000 of shareholder equity, your return on equity (ROE) is twenty percent. $2,000/$10,000 = 20% So return on equity measures the amount of earnings generated on your existing capital base (your plant, equipment, brand names, etc.) Historical Return on EquityHistorically, return on equity has averaged approximately 12% per year for the average American corporation. This means that every $100 in shareholder equity generates about $12 in earnings. Not bad. So how does this effect you as an investor? Good question... ROE: The Economic Engine of a BusinessManagement's ability to generate a high return on equity will directly impact the growth potential of your company's earnings. And growing earnings translate into more profits, more dividends, and hopefully a higher share price for you. How does return on equity accomplish this feat? Another good question... It's like compound interest in a bank account. Every time your company retains a portion of its earnings, it adds those retained earnings to the existing shareholder equity. If management generates the same return on equity as the previous year, then earnings will increase. And increased earnings is one of the key factors we're looking for, right? For example, let's say Company A has the following characteristics: Shareholder Equity: $10,000 Now, let's say Company A takes its earnings and pays out 50% of them to shareholders, while reinvesting the other 50% back in the company. This is what such a scenario would look like:

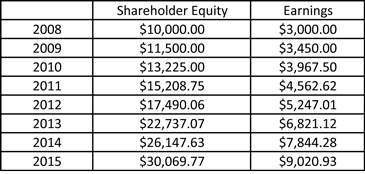

See the correlation between return on equity and earnings? In this case, the company retained 50% of its earnings and earned 20% on them. This resulted in 10% annual growth in earnings. But if the company had retained 100% of its earnings and earned 20% on them, the result would have been a 20% annual growth in earnings. Earlier I stated that the historical return on equity for the average U.S. corporation is approximately 12%. Want to know a little known secret about successfully investing in the stock market? Here it is... Don't be average. If the average return on equity is 12%, then aim higher. And the higher, the better. But, as a general rule, you shouldn't settle for anything less than 15%... ROE and Management EffectivenessSo how does return on equity measure the effectiveness of management? Simple. It tells you whether or not a company's management is a good steward of your money. For instance, let's say your company generates a 7% return on equity. If you can get an 8% return on a AAA bond or a U.S. Treasury, then you want company management to pay out as much as possible in dividends or to find better business opportunities... Why? Because for every dollar in earnings retained by the company, you're only getting a 7% return on your investment. If you can get an 8% return with an alternative investment, but all the company can get you is 7%, then only two real possibilities exist: a) The business isn't a good one In the first case, a poor business (such as one with no competitive advantage) is simply incapable of earning a higher return on equity, regardless of the efforts of a great management team. Hopefully, you'll avoid buying into such a business altogether (or, if the company's competitive advantage has disappeared since you bought in, you'll have the good sense to abandon ship). In the second case, the poor decisions of management are costing you. Management is either making bad decisions regarding business operations, such as acquiring non-complimentary businesses with no competitive advantage... Or, management is retaining more earnings than it should, and making poor decisions in regard to how much of the company's earnings should be paid out to shareholders. In either case, you need re-evaluate your decision to be an owner of the company. You should own only great businesses with high returns and management teams that put their shareholders first. Above Average Return On EquityBecause return on equity so directly effects the future earnings of your business, you want to find and own only those companies that consistently generate above average returns on equity. Why? Because that's the path to above average investment returns as well... For instance, we already saw that Company A, earning a 20% return on equity and retaining 50% of its earnings, was growing its earnings by 10% on an annual basis. But what would happen if a company had identical characteristics, but generated a 30% return on equity? Let's say Company B has the following characteristics: Shareholder Equity: $10,000 Just like Company A, Company B pays out 50% of its earnings to shareholders via dividends, while reinvesting the remaining 50% back in the company. This is what such a scenario would look like:

Look at earnings in the year 2015? They're $9,020.93. For Company A, they're $3,897.43. That means Company B's 30% return on equity, which is only 50% better than Company A's 20% return on equity, generates 2015 earnings that are 131.45% greater! Think of the difference that would make for your portfolio... Is that the type of market beating return you'd like for your Roth IRA? Then invest only in companies with consistently high returns on equity (ROE)... How to Find a Company's Return on Equity All right, so you've determined that you need to invest only in companies with high returns on equity, right? So how do you find out if a company generates high returns on equity? That's a good question... Remember when you were researching your company to find out if it has a track record of consistent and growing earnings? Go to the same place - the Value Line Investment Survey. Your local library should have a copy of the Value Line Investment Survey. Look up the company in question. Just as the profile page on your company provides a list of earnings for the past ten years, it will also list the company's returns on equity for each of the past ten years. Look to see if they're consistent. Look to see if they're above average - at least 15% If they are, then you're one step closer to verifying a great investment opportunity, right? Well, not always... Beware of DebtWhile a high return on equity is usually a sign of a great business, it can sometimes be deceiving. Why? Because return on equity can be manipulated. Not in a sinister or deceptive way, but it isn't always indicative of greatness. Let's go back to Company A. Again, Company A has the following characteristics: Shareholder Equity: $10,000 50% of earnings are paid out to shareholders in the form of dividends, while the rest is retained by the company for internal investment. Now, let's suppose that Company A takes out a loan for $10,000 to purchase a new assembly line, and the new assembly line results in a 50% increase in earnings. Since the new assembly line (asset) is carried on the books at the same value as the $10,000 loan (liability), the net effect on shareholder's equity is zero. But, at the same time, earnings increased 50%, so Company A's revised characteristics look like this: Shareholder Equity: $10,000 A 30% return on equity is superior to a 20% return on equity, right? Not always. In this instance, Company A incurred long-term debt ($10,000) equal in value to the entirety of shareholder equity ($10,000). This isn't necessarily bad as long as Company A can service its long-term debt at a reasonable rate. But, over time, Company A will have to pay back the $10,000 loan. And doing so will take a bite out of its future earnings, making its future returns on equity decline. That's why it's vitally important to evaluate a company's returns on equity over a long period of time. Ten to fifteen years if possible. Otherwise, you might be seduced by an above average one-year return on equity resulting from a large amount of new debt. And that's the next factor you need to address when evaluating a company's investment value - its indebtedness. And, as is always the case - the less debt, the better... Learn About Factor #3 - A Low Debt to Equity Ratio >>> ***z-affiliate-ad-2.shtml*** Return to the top of A High Return On Equity (ROE) Return to Trading Stocks In A Roth IRA Return to the Your Roth IRA Website Homepage

|

What's New?Read 5 Reasons Why I Love My Roth IRA, our part in the Good Financial Cents Roth IRA Movement! Start planning ahead for next year by checking out 2017 Roth IRA contribution limits, and stay alert to this year's changes to the 2016 Roth IRA contribution limits. Our family fully funds our Roth IRA with this website. Learn how you can do it too. Are you confused or frustrated by the stock market? Learn how to build real wealth selecting individual stocks for your Roth IRA... Read more about what's new on the Roth IRA blog.  Hi, I'm Britt, and this is my wife, Jen. Welcome to our Roth IRA information website! This is our humble attempt to turn a passion for personal finance into the Web's #1 resource for Roth IRA information. But, believe it or not, this site is more than just a hobby. It's a real business that provides a stable and steady stream of income for our family. In fact, because of this site, Jen is able to be a full-time stay-at-home mom and spend more time with our daughter, Samantha. But you want to know the best part? ...You can do the same thing! Anyone with a hobby or a passion (even with no previous experience building a website) can create a profitable site that generates extra income. If you're tired of solely depending on your job(s) for family income, click here now and learn why our income is increasing despite the financial crisis and how we're making our dreams come true. |

|

Search This SiteRoth IRA Basics

More About Roth IRAsRoth IRA ResourcesAbout Your Roth IRALike Us On FacebookFollow Us On Twitter

RSSDisclaimerThe information contained in Your Roth IRA is for general information purposes only and does not constitute professional financial advice. Please contact an independent financial professional when seeking advice regarding your specific financial situation. For more information, please consult our full Disclaimer Policy as well as our Privacy Policy. Thank YouOur family started this site as a labor of love in February 2009, a few months after our daughter was born. Thank you for helping it become one of the most visited Roth IRA information sites. Thank you, too, to the "SBI!" software that made it all possible. We hope you find what you're looking for and wish you much continued success in your retirement planning! |

||

|

| ||